Calgary & Alberta Best Mortgage Lending Rates

Due to fluctuating financial markets, mortgage rates in the Calgary area change often! Contact us today to receive current rates and a complimentary in-depth quote and overview of current market conditions affecting the mortgage market.

> Calgary Alberta Best Mortgage Lending Rates

> Okotoks Alberta Best Mortgage Lending Rates

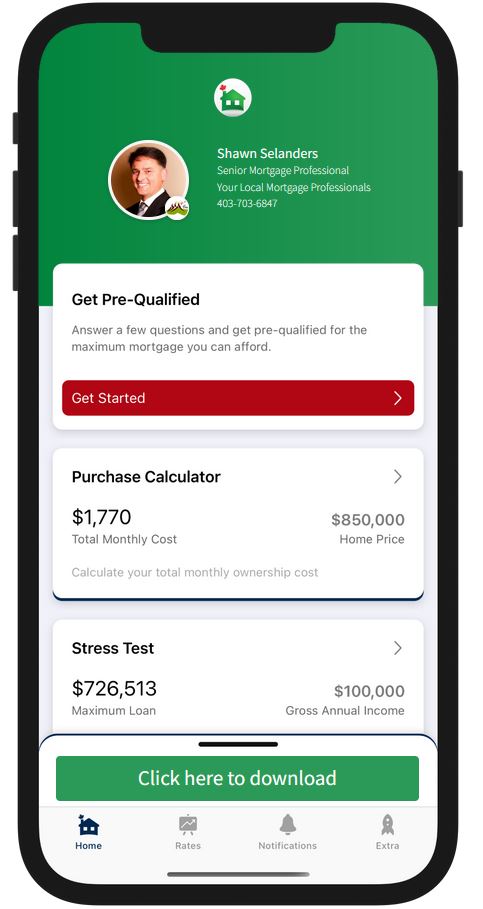

Download my Mortgage App!

There are many features on my app that you'll find useful, including a Stress Test Tool, an extra payment analyzer,

a compare side by side feature to analyze possible scenarios and instantly see differences in interest.

You can also check out the latest rates and even make a request so I can find you the best mortgage product and the best rate that applies to you.

It's easy, fast and free.

If you have any other questions, feel free to contact me by email or phone or click on my picture in my app for additional ways we can connect.

What can you do with my app:

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

Free Mortgage Evaluation

Quick Mortgage Links

Corporate Office - Your Local Mortgage Professionals

Broker | Copyright © 2016